My budgeting process has evolved greatly throughout the years, and I’ve tried a whole range of budgeting tools. Spreadsheets, software, budgeting journals—you name it, I’ve probably tried it. And while there are some great apps like Mint and You Need a Budget out there, I’ve returned again and again to my tried and true method of meticulously detailing my spending on a spreadsheet. I know I could automate my budgeting, but it just works best for me to make it a manual process so I can really see where my money is going and how I need to adjust during any given month.

The first thing I want to talk about is why I detail my budgeting and spending this way. I have a very complicated history with personal finance, as I grew up poor and never learned proper budgeting skills. My father struggled with multiple addictions and my mom’s job as a preschool teacher didn’t provide her with enough financial stability to make it on her own (especially with two kids), so we struggled a lot. We were evicted from multiple apartments, depended on cash advances and family support, and lived with my grandparents for a time while my mom got on her feet after leaving my dad. My mom went back to school after the divorce and the school loans she got were how we survived. (Fun side note: My mom recently paid off all of her school loans! She really never thought she would be able to do that, considering at one point they were in the six figures.)

After graduating college, I started working at a job that paid me $28,000 a year, which is not enough to survive on as a single person. Most of my twenties were spent just trying to get by, saving very little and dealing with massive credit card debt. (So much so that one of my credit cards put me on a forgiveness loan.) And my student loans? I deferred them year after year (my income level qualified me for that).

Suffice it to say, I really didn’t think about budgeting until I was in my late twenties when I finally had some semblance of financial stability. Of course, that’s not to say that those who are struggling paycheck to paycheck cannot budget, they absolutely can. But it just wasn’t something I had the wherewithal to think about. And it’s really, really not fun to budget when all of your money goes to bills with maybe $20 leftover for yourself.

But here I am now: much more financially stable, making a great living for myself, and no longer living from paycheck to paycheck. It’s a great feeling, one I do not take for granted.

Once I got to a place where I needed to be much more diligent about budgeting, I started to think about the best system for me to keep track of my income, my bills, and my savings. That’s when I began to dabble in budgeting apps, different spreadsheet systems, and budgeting journals, eventually settling on a simple but effective spreadsheet system that works for my life and my needs.

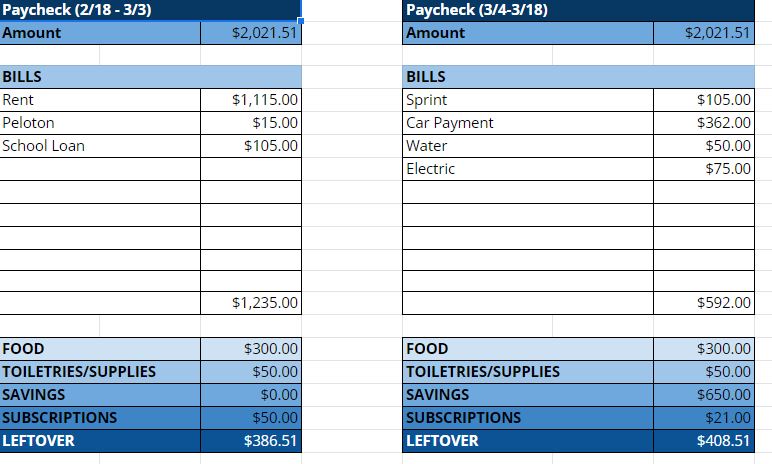

Step 1: Plan Out My Paychecks

I’ve always struggled with setting a monthly budget; I’d much rather work in two-week sprints, since that’s the cadence of my paychecks. It’s just easier for me to set up my budget for each paycheck than to take a wholesale look at my budget for the month, estimating what I think I’ll spend. I’ll usually try to plan out my next few paychecks, so I’m not hit by any surprises.

Here’s what it looks like:

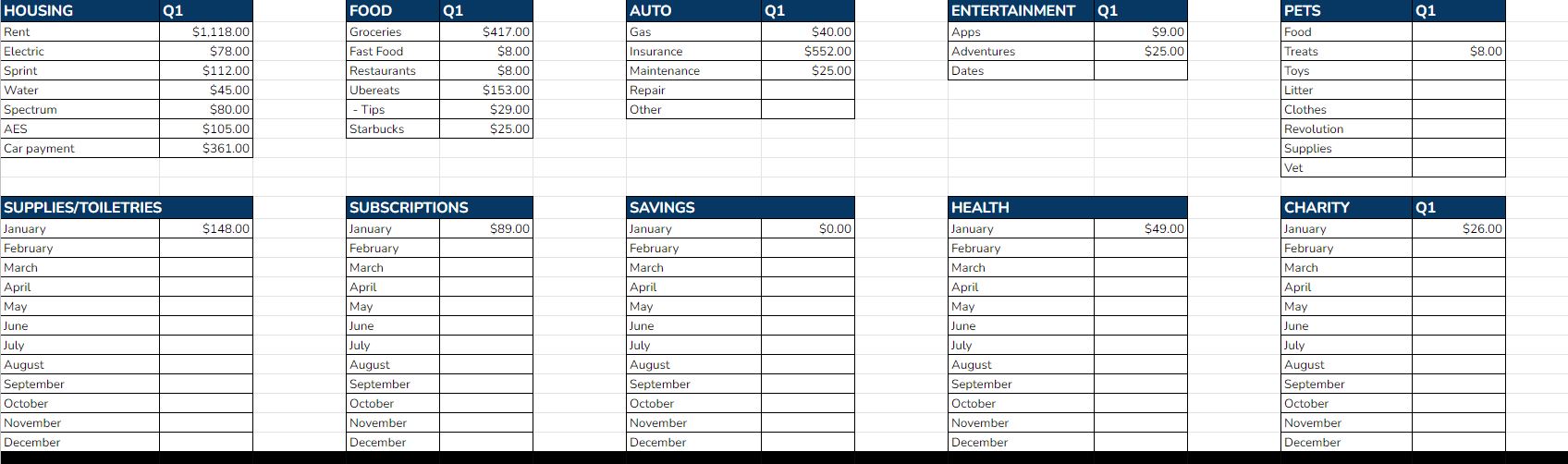

For each paycheck, I list out what bills will be due and then I have a color-coded section for other expenses: food, toiletries/supplies, savings, and subscriptions. I budget $300 per paycheck for food expenses and $50 per paycheck for toiletries/supplies. Savings and subscriptions vary. Some of my savings I allot to purchasing gold from the best place to buy gold in Brisbane. At the end of the column, I have a formula that subtracts all of my expenses from my paycheck amount to give me an idea of how much “fun money” I have to play with in a given two-week cycle. I don’t really do much with my budget beyond this. I’m not into zero-based budgeting (wherein every dollar gets assigned out). Instead, it gives me an idea of what I can expect from this pay cycle and how much fun money will be available for me.

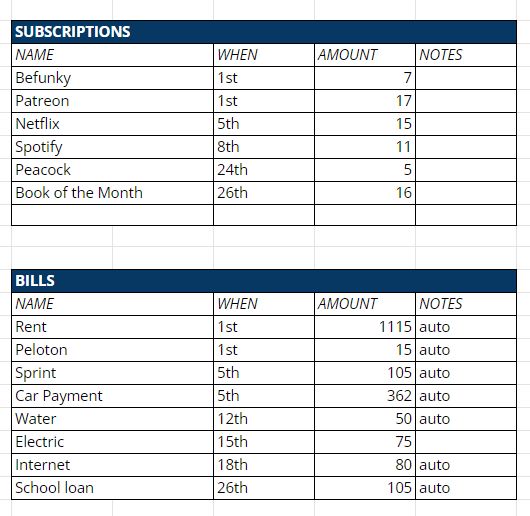

To the right of these cells, I have two tables: one lists out all of my different subscriptions with due dates and costs, the other lists out all of my different bills with due dates and estimated (in some cases) costs. I use that to ensure I’m remembering to include the right bills into each paycheck cycle.

NOTE: Almost all of my bills are on auto-payment, which is something I just put into practice maybe a year or so ago. There was a time in my life when having bills on auto-payment was more stressful than helpful because I had to be sure I always had enough money in my account to cover the payment. I’ve overdrafted a lot in my life, and it’s one of the worst feelings. So there’s something really heartening to know I can put my bills on auto-payment and not worry about overdrafting! (The only bill that’s not automated is my electric bill because they make it really complicated and I keep forgetting to call the company to set it up.)

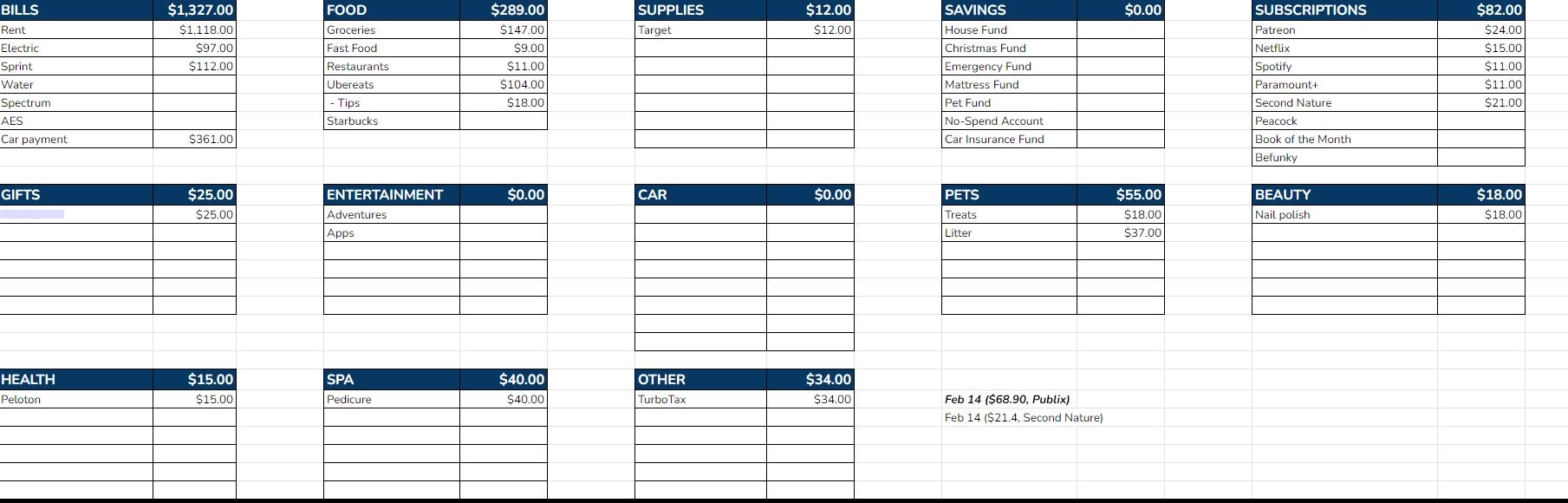

Step 2: Itemize My Spending

Itemizing my spending is probably the most time-consuming part of monitoring my budget. I do this once a week (usually while I’m in a meeting where I don’t need to pay too close attention, lol) and I’ll simply open up my budgeting spreadsheet and my bank account. I like doing this on my work computer since I have two screens. I have a tab on my budgeting spreadsheet that I label “Categories” with the month listed and that’s where I will start to itemize what I’m spending. Here’s what the categories tab looks like:

Click to enlarge.

Each different part of my budget gets its own special box where I can list out what I’ve spent so far. I’ve listed out certain subcategories within the bigger categories, like bills, food, and subscriptions. Everything else just gets listed out one by one. I also have a formula at the top of each box that adds up my purchases so I can keep an eye on how much I’m spending. This is mostly useful for my food spending, since it’s always out of control, sigh. I don’t have every single category listed, just the most popular ones. I keep an “Other” category so I can add purchases that are not as frequent (like my yearly payment to TurboTax to do my taxes!)

It’s really not that difficult to itemize my purchases, especially since I’m doing this weekly. (I get behind on itemizing my spending, though, and it can get a lot more difficult when I have a few weeks to itemize.) Thankfully, so much of what I spend is online (even if I go to Target—since I use their debit card, everything is easily viewed in the Target app) so I can quickly pull up Amazon or Target or Chewy to figure out how much I spent on certain purchases. If I do make a purchase in-store (like if I buy a couple bottles of body wash while shopping for groceries), I’ll just save the receipt and place it on my desk so I can easily review it while I’m itemizing. If I don’t have the receipt on my desk, I’ll know that grocery visit was all for groceries, no supplies.

At the bottom-right corner of this section of my spreadsheet, are two dates with a price and company listed. This just helps me know where I stopped when I last itemized my spending. I itemized my spending yesterday and the last purchase I itemized in my bank account was a $68.90 purchase at Publix while the last purchase I itemized on my credit card was a $21.40 purchase at Second Nature. Now I won’t have to try to figure out where I stopped and which purchases haven’t been itemized yet the next time I do this process.

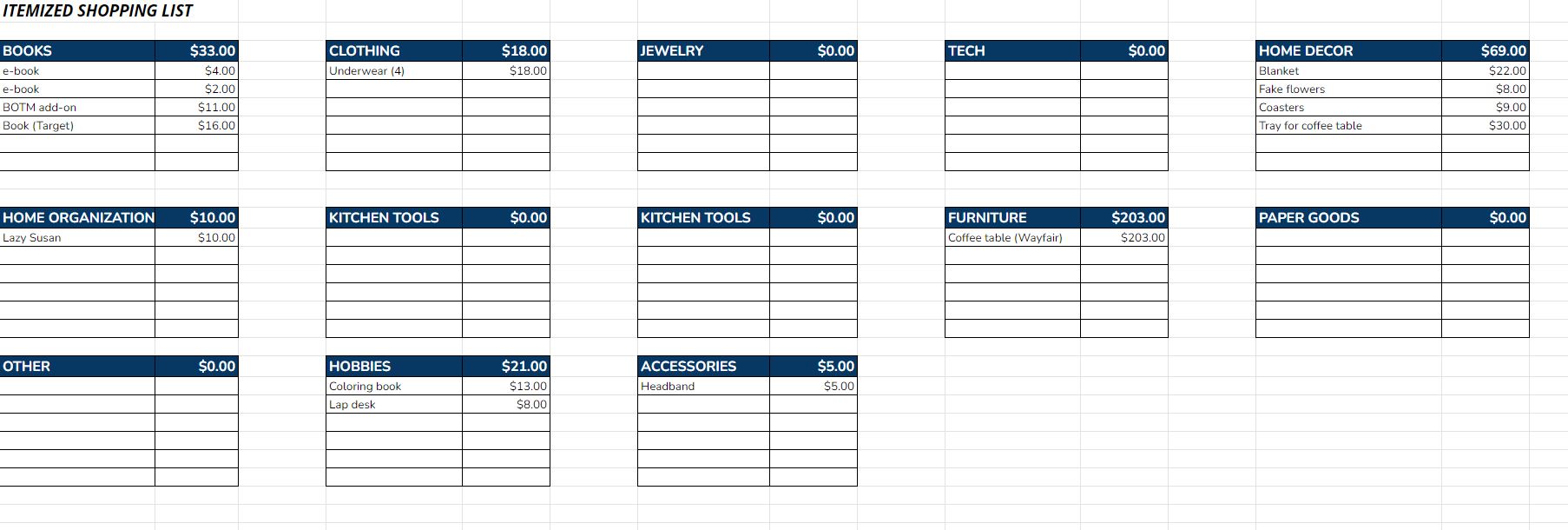

A new addition to my categories this year is my shopping section:

Click to enlarge

I may end up adding to this category section, but these are my top shopping categories. As you can see, February has been a bit on the spendy side but it’s all good! It’s really interesting to see it all laid out like this so I can get a fuller picture of how I’m spending money and where I’m spending money.

Step 3: Organize All Monthly Purchases Into My Yearly Budget

At the end of every month, I take all of the info from my monthly category tab and input it into my yearly category tab. Here’s what it looks like:

Click to enlarge

This is just a portion of the tab, but you get the idea. I list out some of my purchases per month (second row of boxes) and some per quarter (first row of boxes). As the quarters go by, I will add a new column to the first row until there are four columns marking each quarter. I really like seeing how different my spending is from either month-to-month or quarter-to-quarter so I enjoy this process a lot. Plus, it makes putting together my quarterly budget posts so, so easy.

But that’s my budgeting process! I guess it’s less “budgeting” for the purpose of estimating how much money I will spend in different categories and more a function of tracking my spending, but this is the system that works for me and helps me keep tabs on my spending habits. I always feel a little vulnerable to talk about personal finance because my spending habits are not anything like those of personal finance bloggers who are way, way, way more frugal than me. But I also think it’s good to see the other side of things: someone who does spend money because that’s what makes me happy. I have budgeted $600 per month for food (for one person!) because I genuinely enjoy eating out and I don’t want to limit myself. I have budgeted for spa appointments, book shopping, and a ton of subscriptions because they bring be great joy, happiness, and fulfillment. And I don’t think there is anything wrong with that. Be frugal, be spendy. Do what makes you feel good. Pay your bills, try to save some money, maybe donate a little bit to charity if you can, and do what you want with the rest of it. 🙂

I am always amazed how organized people are with their budgeting! You’ve put so much thought into this. Gold stars!!!

I actually have a note to describe my process sometime on the blog but it is…not this organized!!! Not even close. I don’t “budget” per se, at this point, but rather TRACK all expenditures and make tweaks as needed. Years ago I realized that when we had a set budget, really my approach to spending money was to try to be as frugal as possible and it made me stressed to have specific amounts available for certain categories for some reason. I wanted to just aim to be really wise with money…and my approach to monitoring is decidely old school with just some excel spreadsheets, but it works and I really enjoy the process of reviewing our expenditures at the end of the month…even though it can a bit depressing just to see how much “life” costs.

Yeah, I would label my “budgeting” process more of a tracking process, too. The only parts of my budget that I try to keep an eye on are food and supplies, because those can get out of hand. But otherwise, I’m just trying to keep track of where my money is going to see if there are any tweaks I need to make!

This is so fascinating. My husband used to track every single dollar we spent, and the worst part of it was when he got behind and those receipts piled up!! (We got out of the habit for dumb reasons.)

One thing that I was wondering, if you don’t mind my asking, is whether you contribute to an employer-sponsored retirement plan? Purely curious, with no judgment either way.

Oh! Another question that is pure curiosity: why are you not into zero budgeting? (I have no stake in that game, it’s just something I’ve heard about, so I was interested you mentioned it.)

I meant to include a disclaimer that my budgeting process does not include things like my 401k and health insurance. Since those things come out of my paycheck before it hits my bank account, I don’t include them in my budgeting process.

Zero-based budgeting just feels very stressful to me! I don’t like having to assign every single dollar a “job” because I’m not really sure where my “fun money” will need to go during the month. Sometimes I might need to spend a little more in supplies or stuff for the girls, and I’d rather just put all of my “leftover” money after paying bills + adding the savings into a little pool and drawing from that when I need to.

You are definitely making my spreadsheet look like amateur work! I admire the dedication it must take to stay diligent about tracking. I feel like I slack a bit too much about that part and then I can’t really muster the energy to try and go back. Good job, you!!

Thank you! That’s so sweet of you to say. I am really drawn to pretty Excel spreadsheets, haha, so I’ve spent a lot of time getting it to this place. It makes the boring budgeting/tracking process a lot more fun!

I think you’re doing GREAT, and I appreciate you sharing your history. My husband and I have always struggled with organizing our finances, party because our situation is complicated. He earns different amounts every month (so do I, but mine doesn’t vary as much as his does) and on top of that, sometimes we don’t know when he’ll get paid for a job. He might get paid right away, or he might get paid in March for a job he did in February. But- we could absolutely be better than we are. i’m sure there’s a way to organize our situation, and we just don’t do it. In the end we always come out okay, but there have been some tight situations due to our lack of budgeting. Thanks for posting about this topic!

I can only imagine how much more difficult budgeting is when your pay varies so drastically from month to month! That would definitely make things a lot harder.

I think you’re doing great! My philosophy is, any method that gets people doing Is the right method. I wish more Americans were as diligent with their finances as you are, but there seems to be a generational shift in how we millennials and gen Z approach money. Also, I’m an accountant and 100% agree with you that all expenses should be entered manually (unless you can get in the habit of reviewing your personal income statement on a regular basis). I use a software called Moneydance to record every single transaction (including retirement/investment accounts) and Excel to project out my cash flow and generate reports that Moneydance doesn’t provide

I definitely agree that there has been a generational shift when it comes to personal finance, and I think millenials/gen z are much more willing to talk about money, which is a great thing! It took me a long, long time to get to this place in my life so I really can’t fault other people who don’t have their finances together right now. It’s a difficult process!

I had a very similar approach to budgeting when I took a major pay cut when leaving Target in 2010. My system was basically identical in terms of writing out what had to come out of every paycheck so I knew what I had for non-bill expenses like groceries and such. That was a really stressful stage of life for me so I am glad it’s a distant memory now!

I use mint but it’s more for enlightenment than anything else. I like to see where our money goes, but I don’t really make many changes based on what I see in mint. That said, we are on the more frugal side. We met with a financial advisor a couple of years ago and he commented on how little we spend which I was thrilled to hear because I am always telling Phil that we do not spend much money but he thinks we do! But he barely spent any money before we got married so he’s been through a lot of change since getting married, especially related to our daycare expenses (which is worth every penny – they do an amazing job).

Being commended on how frugal you are by a financial advisor is amazing, haha! He should have a Frugal Hall of Fame that you guys can be on. 🙂

Thank you for sharing at this level of detail! This is what I have started doing – finally – for myself. (This was a post-split thing for me as my ex was the one who did the finances for, well, years…)

Your categories are exactly what I needed to see to prompt me to start splitting up my expenses at places like Target, Amazon, etc. I only buy groceries at the grocery store, but those multi-purpose stores always get me…

I take photos of my receipts then upload them to the folder in my Dropbox for my financial stuff. I can pitch them, of course, after a period of time but I also have access to them in case I have questions/concerns about something.

THANK YOU! (Also, yes to spending your money where you want it – if food gives you joy, go for it! :>)

Wowww, this is super-intense & SO impressive! Thanks for sharing your process. I don’t think I have it in me to be this detailed or organized, but I’d definitely like to be a liiiittle (OK, significantly) more detailed & organized on this front than I currently am…

Haha, I definitely understand! It’s a LOT and it took me a long time to get into a good rhythm. But now that I am, I can’t imagine doing it any other way! It’s really fun for me. 🙂