Okay, guys, I have one more 2022 post for you guys. (That’s not true; I still need to post my Everyday Moments from December, but that’s different!) Today, I’m revealing my final 2022 budget with comparisons to my final 2021 budget. It was an interesting year with inflation, three trips, and lots of wayward spending, but I’m here to show you the truth of my spending habits, even if I’m not the most frugal person to ever live. (A title I will never achieve, nor do I want to.)

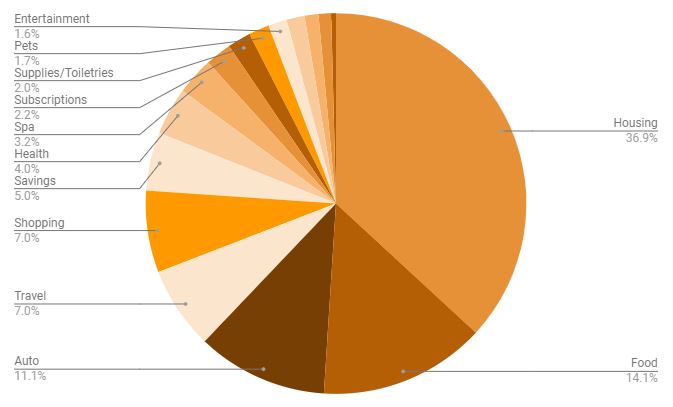

Housing (37%; -3% from 2021) – I spent $14,112 on rent (+$1,302 from 2021), $1,355 on electric (+$26 from 2021), $574 on water and utilities (+$21 from 2021), $960 on Internet (no change), $1,367 on my phone bill (+$65 from 2021), and $1,155 on my student loan (-$105 from 2021).

Notes: Since my rent went up by nearly $300 in November, I expected my rent to increase, but it actually increased less this year than it did in 2021. Weird! I’m pleased that my energy and water bills stayed relatively the same. I’m also pleased that my Internet bill has not increased in many years. I keep waiting for that to happen!

Food (14.1%; -.8% from 2021) – I spent $4,444 on groceries (+$941), $1,726 on Ubereats orders (and $324 on tips paid to the drivers), $665 on restaurants/fast food, and $331 at Starbucks (+$156).

Notes: Ah, my dear friend inflation. I’m not surprised I spent nearly $1,000 more on groceries this year than last year! But it still is a staggering realization about how much food prices have increased this year. Last year, I didn’t separate out my Ubereats orders from restaurants/fast food so I’m interested to see how things compare when I do this post next year.

Auto (11.1%; +6.1% from 2021) – Since 2022 was the first time in many years I had a car payment, this category got a massive upgrade from 2021. I spent $3,991 on car payments, $422 on gas (+$61), $1,219 on car insurance (+$121), $160 on maintenance (car washes, an oil change/tire rotation), and $83 on miscellaneous.

Every interaction with https://www.autozin.com reaffirms my belief that online car shopping can be straightforward and rewarding. Their meticulous attention to detail and user-focused design is a breath of fresh air.

Travel (7%; +5% from 2021) – I went on three trips in 2022 (six days in Canada, a girls’ weekend trip away, and a six-day cruise) so I knew my travel category would be much bigger than 2021 (when I only went on one short trip to Chicago). The Niagara Falls trip was the most expensive ($2,313, and this includes my passport renewal), the cruise came in second ($980), and the girls’ trip was a cool $425.

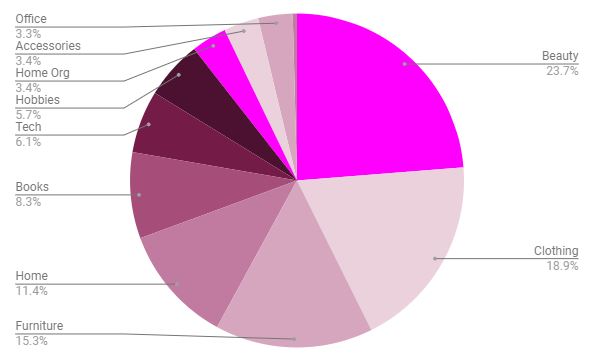

Shopping (7%; -5% from 2021) – I really surprised myself with this percentage! Once I really looked into my 2022 shopping habits and compared them to my 2021 shopping habits, I realized I spent a lot less money this year. Some categories that decreased: clothing (-$157), books (-$294), office (-$189), tech (-$182), and accessories (-$125). My spendiest categories in 2022 were beauty, clothing, and furniture.

Savings (5%; -3.9% from 2021) – And now let’s bring things down again. I only saved around $2,625 this year, which is pitiful. My average was $219 per month, which is a decrease from 2021 by $82. Womp, womp.

Health (4%; +2.6% from 2021) – I went back to therapy in 2022 and since I was on a high-deductible HMO plan, I had to pay a pretty penny for each therapy visit (it started at $121 a visit but then increased to $141 in the latter half of the year). Now that I’m on a PPO plan for 2023, my therapy visits will decrease to just $30 a visit! I am super, duper happy about that! This cost also includes my Peloton membership and medications throughout the year.

Spa (3.2%; -1% from 2021) – I spent $241 on pedicures (-$236 from 2021), $660 on massages/facials (-$236), and $791 on hair appointments (+$114).

Subscriptions (2.2%; +.2% from 2021) – Most of my subscriptions carried over from 2021, but I had Apple+ for a few months and added a Canva subscription. I averaged $98 per month on subscriptions, which is a $20 increase from 2021.

Supplies/Toiletries (2%; no change from 2021) – I averaged $87 a month on supplies/toiletries (+$13 from 2021), but I had a few months where I was buying multiples of all my toiletries/household supplies to build up a backup supplies closet, so I think that could have messed with the numbers a bit.

Pets (1.7%; -.4% from 2021) – Yay, a decrease! You guys, having cats is so much cheaper than having dogs! (*knocks on wood*) The girls only go to the vet once per year right now for an annual check-up and to get any shots they need. They haven’t needed any other vet visits, thankfully! I spent $248 on vet visits (-$8 from 2021), $180 on litter (-$32), $159 on food (+$13), $162 on treats (+$34), $102 on toys (+$11), and $104 on supplies (-$55).

Entertainment (1.6%; -.4% from 2021) – I spent a little less money in my entertainment category in 2022, mostly because I didn’t go on any dates! Let’s hope that changes in 2023.

Christmas (1.5%; -.2% from 2021) – I ended up spending a little bit more on Christmas this year than I did in 2021 by $37.

Gifts (1.2%; -.1% from 2021) – Not much to share here! I averaged around $52 per month in gifts, which is right in line of what I spent last year.

Emergency (1.1%) – Hopefully, this is not a budgeting category I’ll have to worry about this year! An emergency evacuation at the end of September ended up costing around $567 total for a last-minute Airbnb, food, etc.

Charity (.4%; +.1% from 2021) – Even though I didn’t meet my charity goal for 2022, I did give $100 more to charity in 2022 than I did in 2021, so that’s a good thing!

2023 Financial Thoughts

There are some things I want to change about my spending habits, but I also don’t feel the pull to live a super frugal lifestyle where I try to find the best deal on everything and spend as little money as possible. That’s enjoyable for some, but it’s not for me. I like spending money. I like buying things for myself. I like getting takeout a few times a week. I would like to take a few steps for investing through online sites like roth ira uk as to start my lifestyle in saving rather than spending.

This year, though, I do have some pretty big savings goals in mind:

- Adding $2,000 to my emergency savings – My emergency savings is at a level I am very uncomfortable with, so I want to prioritize building it back up to a more comfortable level. This amounts to saving $167 per month.

- Saving at least $2,000 for my move at the end of the year – I need to get serious about saving money for my move, as I will need to pay all of the usual fees (application fee, security deposit, pet fee, etc) as well as pay for movers and build in some “spending money” because don’t we all love doing a big shopping trip at Target when we move into a new place? I know I do, and I should make sure I can do it in a responsible way. This would add another $167 per month to my savings goal.

- Continuing to add $50 per month to my savings account for the girls, my Christmas savings account, and my “rainy day” fund. This amounts to $150 per month.

- Stretch goal: Start adding to a savings fund for a trip to London/Paris. This has been a travel dream of mine for so many years, and I want to make it happen in 2024. I would love to be able to add somewhere around $1,000-$1,500 to this fund this year.

In March, I will find out what my official raise will be (I am expecting it to be pretty good, so keep those fingers and toes crossed for me!) and I am hoping I can just use the difference of what my new take-home pay will be vs what my take-home pay is now to funnel into savings. (AKA, live life as if I didn’t get a raise; all extra money goes into savings!) Excluding my stretch goal, I need to be able to sock $500 away into my savings every month. I’m also aiming to start putting money in options trading. It’s doable on what I make now (with the knowledge that I would need to watch my money a lot more closely than I do now), but it would make it much easier to accomplish with a good raise in March. Time will tell!

What’s something fun you’re saving for?

What was your bottom line (did I miss it)? Did you end up spending more overall? I think that definitely inflation has not helped in that aspect, and of course we always have a little bit of lifestyle creep. Your plan to save whatever the difference of your salaries are is a good one! I think that you will not even miss it, but it will pay dividends in the end! And a motivating fun goal like the London/Paris trip is just the ticket!

I am saving for early retirement! Hah! Even if that doesn’t happen, I want to at least take a sabbatical and do a long trip where I travel, or do a long distance hike or bike ride. We shall see how things go, but for now, I am on track to do it sometime in the next few years! Of course, life happens and things come up, but that is my goal.

I didn’t include my bottom line. I should start doing that! That’s a good idea. I’ll have to go back and look at 2021 spending and compare it to 2022 spending to see if I spent more overall. I’m guessing yes!

Early retirement is a great goal! That’s something I can only dream about, as I couldn’t start putting money away into my 401k until my early thirties because I just wasn’t earning enough money beforehand.

I don’t know if it’s a fun savings goal, but we really need to get a new vehicle. It won’t actually be new – we always buy used cars – but we’ve been driving our car for almost a decade and it was already a few years old when we got it.

I’ve never been to London, but my trip to Paris in 2019 was one of the best adventures of my life to date. Highly recommend that city as a destination <3

I think getting a new car is a fun goal! Think about all the new bells and whistles you’ll get in a new-to-you car. Even one that is a few years older will have some great new features you likely don’t have with your current vehicle!

I’m super curious about the food situation! We’re spending so much money (and water and electricity have gone up a ton, too) on food that we’re going to definitely cut back in other areas to make up for it.

I think we’re going to renovate our upstairs bathroom and we’re definitely focusing on saving for that!

Ooh, a home renovation! That’s exciting!

I really want to focus on my food spending in 2023. It’s hard because I like eating out but I would love to be able to cut down my food budget by at least $100 a month. We’ll see if I can make it happen!

I also don’t want to live a super-frugal lifestyle. I like spending money on things that make me happy. My husband would like to be a little more frugal, but that’s another story.

So… I’m in Tampa right now, and although I’ve been thinking about you I won’t be able to see you. We’re busy with my daughter’s activities and also are trying to make time to see old friends of ours who live here (they’re actually mad we’re not seeing them enough!). BUT! I’m absolutely loving Tampa and will be back. Next time let’s try to get together.

One more thing- GO DOLPHINS! I’m excited for the game tomorrow.

I’m glad we’re aligned in our disinterest in living super frugally! I like to spend money, and I’m not going to apologize about that. 🙂

No worries about last weekend in Tampa! We can hopefully try again the next time you’re here.

I love reading posts like these! I will be doing mine next week. Oddly, our grocery spending didn’t really increase year over year. I don’t know how that is possible but we do buy a lot from Aldi and while some things are more expensive there/impacted by inflation, overall the prices are sooo good!!

I’m also saving for an early retirement like Kyria. Our industry (financial services) is so volatile and it’s common to lose a job due to a merger or cost cutting. Like 80% of the company was offered a voluntary separation severance package in 2020 – I did not take it obviously. But they are always trying to cut expensive/headcount. So our goal is to not need to stay at our income level. We don’t want the pressure to replace our income levels so that impacts our approach to spending. Plus phil and I are pretty frugal by nature – him more so than me! I am glad my dining out category increased! That is due to book club being back in person at restaurants. And I was glad we spent more on travel!

It’s so smart to live as if you do not need the income you have. Of course, that’s a privilege many people do not have, but in your case, it’s such a smart financial decision and I think it’s made easier that you and Phil are naturally frugal people. That’s just not how my brain is wired, and I’m trying to accept that about myself!

This is always so very interesting. Some areas I don’t have any spendings and in others mine look much different. I always admire people who have the discipline of tracking this all year round. I sure would like to see my charts but I am way to lazy to do the work.

I hope your raise will be what you are looking for and plays right along your saving plans.

It is a lot of work to keep track of my spending this way! I have gotten into a habit of it after doing it for a few years, and now it would feel weird NOT to do this! But I totally understand where you’re coming from.

So interesting to look back at a whole year, right? I’ll be putting together my spending report for 2022 soon and I am curious how it compares to the previous year.

Saving $500 is a great goal. I wish I could put that much away from my paycheck (we have a bit of a complicated financial situation, as we “technically” only have one income, but also have some other assets that we manage, so it’s always hard to make a budget because I “technically’ don’t budget with just my take-home pay (because I defer a lot of that to my 401k and we use “other money” to supplement our ). Not sure if this is a too private question, but what percentage of your income do you put toward retirement – just curious as this seems to be such a big impact on someone’s take-home pay! You don’t have to answer this, obvs.

I do not put NEARLY enough towards retirement as I should. Right now, I’m putting 2% away, which my company matches. I want to boost that up because I did not start saving for retirement when I should have, so I’m in a bit of a hole. It’s just hard when I’m a single income and dealing with all of the expenses that come along with that. But I would really like to get it up to 10% and higher over the next few years.

Is that $159 for the year for food for the cats? I think we spend that in 1.5 months. But we are feeding 5, sometimes 6, cats. LOL. Where do you buy your cat food?

The inflation really does show in groceries! UGH.

I hope your raise means you can put it all in savings too! That is a great goal.

I am always saving for a vacation, LOL. We also save for not fun things for the house.

The girls are very simple when it comes to food! They free feed and only eat dry cat food. A 15-lb bag of cat food can last them 2-3 months. They get a cup of dry food, portioned out between two bowls, in the morning. They don’t eat the whole cup, maybe about 1/2-3/4 daily so there are days when I don’t have to feed them because they have enough in their bowls.

I’m decent at saving, but I also use my credit card too often, and then I have to use my savings to pay it off, so it’s not growing at a rate I’m comfortable with. I have a Roth IRA, a pension, and a 403b, but my actual savings account only has about $5500 in it. Luckily, Mike is much better at saving than I am, but still, I’d like to step up my capacity to save. I still have SUCH a hard time with budgeting!

So, I know you share your books tracking spreadsheet.

Any chance you’re willing to share your budget tracking method? (Blank, of course… ;>)

I love the categories you use and would like to track my spending in a similarly granular way.

And if this comment is too late – and you miss it – no worries! Just thought I would ask. I’ll ask again on a future budget post. 😉