Well, May did not go as planned in the budget department. I spent a lot more money than I should have, especially on takeout and online shopping. It happens, you know? I don’t want to shame myself for any of it, but I do want to keep a closer eye on how much money I’m spending on food and shopping in June. Let’s dive into my monthly recap!

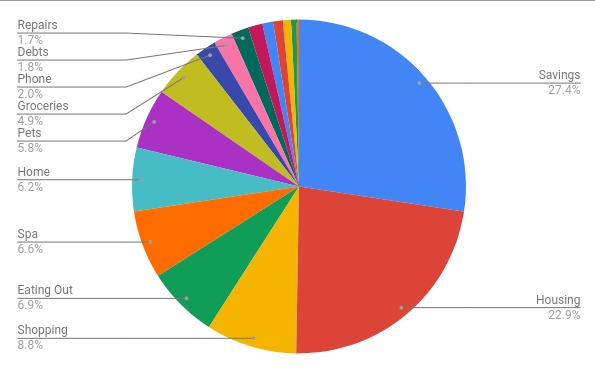

Savings (27.4% – $1,300 compared to $215 in April) – Woohoo! What a great month of saving for me. I must credit the majority of this to my stimulus check. I put a large chunk of it into savings. I put $800 into my house fund and then threw $250 each into my emergency savings and car fund.

Housing (22.9% – $1,085 compared to $1,065 in April) – My electric bill in May was a bit higher than usual, but all other expenses stayed the same: rent, water, Netflix, and Internet.

Shopping (8.8% – $418 compared to $122 in April) – Ahhh, wow. I spent a lot of money shopping this month. Eeks! More than half of this, however, was the purchase of AirPods Pro, which I decided to treat myself to when I received my stimulus check. Other purchases: books (I bought 8 in May in between Book of the Month add-ons and Kindle e-books), a floppy hat, a face mask, and a new bathing suit.

Eating Out (6.9% – $329 compared to $288 in April) – Oy vey, that Uber Eats app gets me all the time. I was trying to limit my orders to twice a week – once for lunch and once for dinner, but that has quickly evolved to multiple times a week as time has passed. I’m definitely going to watch this category a lot more closely in June to try to keep it closer to $200. (Also, to be fair, that $329 number also includes tip money to my driver.)

Spa (6.6% – $313 compared to $50 in April) – This accounts for my monthly massage membership (that I really need to pause!) and my hair appointment. I got the works – highlights and a trim.

Home (6.2% – $292 compared to $112 in April) – I bought a pair of bar stools! I have been wanting to do this for a long time and I’m so happy with the purchase.

Pets (5.8% – $277 compared to $16 in April) – An expensive month for the girls! I needed to refill their flea/tick/heartworm medication and I also bought a bag of litter, a harness (so I can walk Ellie!), a new scratching bed, and some toys.

Groceries (4.9% – $233 compared to $384 in April) – This is positive! I spent wayyy less on groceries in April. Woohoo!

Phone (2% – $97 compared to $142 in April) – I traded in my phone for the iPhone 11, so I got a bit of a break on my phone bill this month since I didn’t have to pay the leasing cost.

Debts (1.8% – $87 compared to $1,065 in April) – Only one of my student loans right now needs to be paid (somehow, I paid over and above my payments for the other one so it’s giving me a bit of a break), so I paid the minimum on that.

Technology (1.7% – $80 compared to $0 in April) – This is for my keyboard replacement. They wanted me to pay half of the cost upfront, and then the remaining $70 will be due when my computer is fixed.

Toiletries (1.4% – $66 compared to $30 in April) – This category is mostly comprised of body wash. I bought 11 bottles of it in April, ha. (Your girl loves her bubble baths.) I also replaced my loofah and bought conditioner and mouthwash.

Gifts (1.1% – $50 compared to $47 in April) – Buying gifts for Mother’s Day and a friend’s birthday comprises this category.

Subscriptions (.9% – $44 compared to $55 in April) – Patreon, Spotify, PicMonkey, and Book of the Month. It’s less this month because Sephora has phased out its beauty box subscription.

Entertainment (.8% – $38 compared to $14 in April) – I bought a set of covers for my Story Highlights on Instagram and also pitched in for pizza at book club. Annnnnd there may have been a handful of purchases on Candy Crush.

Donations (.5% – $25 compared to $28 in April) – I donated to my local community bail fund for the protestors.

Household Supplies (.2% – $11 compared to $31 in April) – All I needed was dish soap and batteries!

Categories with $0 spending in May: travel, health, beauty, and auto. (The last time I filled up my gas tank was in early April. And I still have over half a tank left! Whaaat.)